Evaluation:

P1. Disagree. Suppose we define "intrinsic value" as "the benefit derived from the minimum functional properties of an asset that are universally recognized and broadly applicable." In other words, "intrinsic value" is the "objective functionality" of an asset. That seems fair, but this definition causes us to dismiss other kinds of value as "worthless" (such as aesthetic or sentimental value), and clearly those types of value are not worthless.

If we expand the definition of "intrinsic value" to include aesthetic or sentimental value, then we've introduced subjectivity into the core value of something. Since subjective value, by definition, is a matter of opinion, and since we cannot make claims about other people's opinions, then the presence of subjectivity prevents us from making claims about this kind of value.

Hence, this latter definition of intrinsic value (that includes subjectivity) leads to a False Premise because it precludes us from making claims about other people's value, and the former definition of intrinsic value (that is strictly objective) also leads to a False Premise because it ignores a very real component of value (i.e. aesthetic or sentimental value).

Either definition of "intrinsic value" leads to a False Premise, so I Disagree with Premise 2.

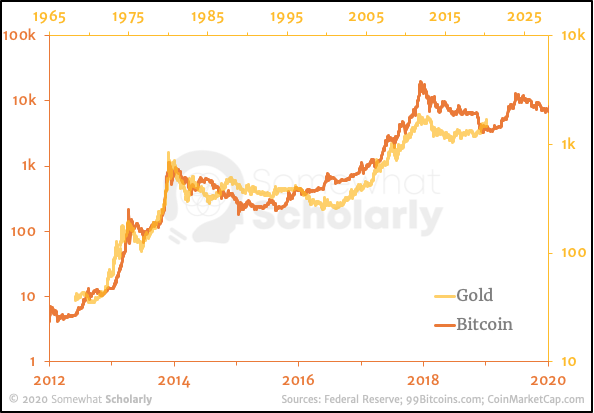

P2. Disagree. Bitcoin does, in fact, have intrinsic value. In order for you to "have" a Bitcoin, the Bitcoin network must acknowledge that you have custody of that Bitcoin (i.e. you must supply a valid private key to claim ownership of a balance in a public address).

If you can demonstrate ownership, then you can transfer ownership - without any additional permissions or paperwork. The two functions (demonstrating and transferring ownership) are "structurally connected."

The intrinsic value of a Bitcoin, therefore, is the ability to establish and transfer ownership of digital assets on a globally-recognized and un-cheatable ledger. In other words, once you own something on the Bitcoin network, nobody can take it away, except you (either your own choice or your own negligence).

Another way to consider this intrinsic value is that each Bitcoin user has the same "power" and "sovereignty" as the other users. There is no hierarchy of power - such as authoritarian governments, remorseless corporations, and powerless individuals - there is only a public address with a private key, and everyone on the network is the same. It is an amazing environment of equality, and it's built into the network - if you "have" a Bitcoin, you "have" this equality.

Therefore:

C3. Disagree.