- Is the Coronavirus dangerous?

- Should we take precautions?

- What effect will the Coronavirus have on the global economy?

February 6th, 2020 Miles Guo’s interview with Mr.Bannon at War Room

Podcast: Play in new window | Download

Subscribe: RSS

February 6th, 2020 Miles Guo’s interview with Mr.Bannon at War Room

Podcast: Play in new window | Download

Subscribe: RSS

Premise 1. In a healthy economy, the Demand for goods and services tends to increase. Premise 2. When Demand for goods and services increases, prices go up. Therefore: Conclusion 3. In a healthy economy, prices go up.

Evaluation:

Premise 1. "In a healthy economy, the Demand for goods and services tends to increase." Dubious. While it's true that Demand tends to rise with income, it's also true that Demand declines with age. In other words, a person tends to Demand less as they get older.

The truth of this Premise is unclear, but let's suppose we Agree.

Premise 2. "When Demand for goods and services increases, prices go up." Disagree. This Premise is true ceteris paribus, meaning "all else equal," but in the real world, it's never the case that "all else is equal."

In a healthy economy (i.e. one in which (1) saving and (2) innovation are both encouraged and rewarded), the Supply of goods and services will tend to increase faster than Demand (because useful innovations will increase Supply, and people can't Demand those new goods and services until after they've been produced, so Demand "lags," or "follows," or moves slower than Supply).

The net effect on the economy (when Demand and Supply are both increasing) is a higher Quantity of goods and services sold, typically at a lower Price (see Chart below).

Therefore:

Conclusion 3. "In a healthy economy, prices go up." Disagree. In a healthy economy,* prices go down.

*[A "healthy economy" is one in which (1) saving and (2) innovation are encouraged and rewarded... via (1) sound money, (2) low taxes, and (3) minimal regulations.]

Evidence:

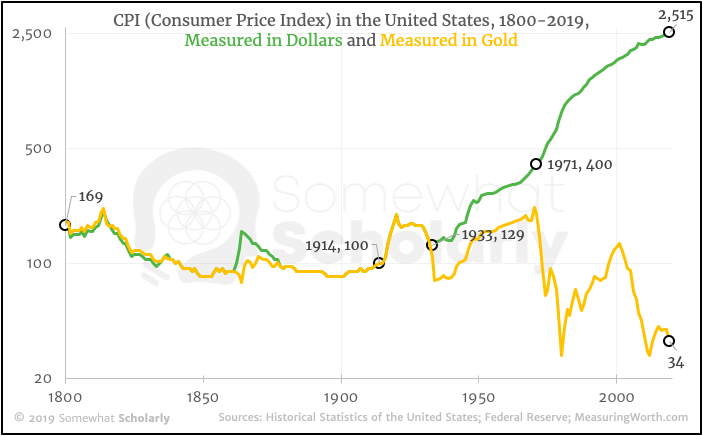

Here's the Consumer Price Index (i.e. the average level of prices) in the United States from 1800 - 2019. As you can see, during the first century (when the dollar was backed by gold), the general trend is downward. In other words, prices go down:

During the last century, the Federal Reserve (a for-profit corporation created in 1913 that acts independently of the government) has printed so many dollars - at such a rapid pace - that it forced the U.S. government to partially abandon the gold standard in 1933, and completely abandon the gold standard in 1971.

The Fed continues to print dollars at an exponential rate, and the effect on the economy is clear: since 1914 (the first year of the Fed's monetary policy), prices have increased more than 25x. [Green line in Chart].

Quite simply, the monetary policy of the Federal Reserve (i.e. printing dollars) has made it much more difficult for the average person to buy things, unless he or she owns gold:

If we divide the CPI by the dollar-price of gold (to measure prices in ounces of gold - i.e. real money that cannot be printed), we find that prices dropped 66% since 1914. In other words: if you own gold (or use money backed by gold), prices go down. [Gold line in Chart].

For those who want to imagine what "falling prices" would actually feel like on a personal basis, imagine that the CPI is actually your monthly rent payment. [You could also imagine that it's the price of a gallon of milk, or a loaf of bread, or anything else that you buy weekly, monthly, or yearly]. Would you prefer that these items cost more every week, or less? (It's not a trick question).

Below is the same CPI data from above, but imagined as a monthly rent payment.

Notice that there's really "no difference" between the dollar-price of rent and the gold-price of rent for over a hundred years (i.e. they both get cheaper, slowly, at about the same rate). This pattern changes abruptly in 1914 (i.e. the first year of the Federal Reserve's monetary policy), when the two prices start to diverge wildly:

If you're wondering why the difference in 2019 doesn't look like 98%... it's because the vertical axis uses a logarithmic scale.

Here's the same graph with a linear scale:

Without a gold standard, a central bank can print unlimited amounts of fiat currency; this inflation punishes people who try to Save money, which in turn creates a mild state of "panic buying" that can last for generations.

If you expect prices to go up tomorrow, you'd better buy something today, even if you don't really need it; otherwise, you're choosing to get poorer.

As an added twist, the economists at the Federal Reserve point to all the "increased spending" (on goods and services that people don't really want) as "evidence" that the economy is "growing," but in reality, this panic buying is a symptom of a troubled economy - not a healthy one.

On a gold standard, however, this "theft by inflation" is not possible. In fact, the average person gets richer (i.e. can "buy more stuff over time") just by Saving money. When prices go down over time, you can afford more tomorrow than you can afford today. And the longer you Save, the richer you get.

But that only happens if you use sound money.

So the question must be asked:

Would you rather live under the Federal Reserve's monetary policy, or on the Gold Standard?

You may also like:

"Gold is not a hedge against price deflation."

Initial Claim:

@25:24 - 26:17

Peter Schiff: "When you buy Bitcoin, it's not providing any service. It's not satisfying any of your needs or desires."

Anthony Pompliano: "It's providing cryptographic security."

Peter Schiff: "But security of what? You've secured nothing. Yes, I mean, I could even concede potentially that... if I own a Bitcoin, no one's going to steal it. But if I have nothing, then what difference does it make whether someone steals it or not? I mean it only has this value to the extent that someone else believes that they're going to get rich by buying it. And again, y'know, you don't want to confuse (because you said earlier that [Bitcoin is] a store of value)- I will concede that the price of Bitcoin has gone way up, buy you can't confuse "price appreciation" with a "store of value." Anything that can go up can also come way down, as we've seen before. I mean Bitcoin has had some spectacular declines, and so there's a lot of volatility there."

P1. If an asset has risen in price because of purely speculative hopes, then that asset is not a store of value. P2. Bitcoin has risen in price because of purely speculative hopes. Therefore: C3. Bitcoin is not a store of value.

Evaluation:

P1. Agree. If an asset has risen in price because of purely speculative hopes, then that asset is not a store of value.

P2. Disagree. Bitcoin has risen in price because of speculative hopes, for sure (and we might call that an "offensive" use case), but Bitcoin has also risen in price because of increasing demand for its utility (which we might call a "defensive" use case):

Bitcoin's utility is appealing to people who have been (or might be) the victim of theft, extortion, censorship, restriction, inflation, marginalization, suppression, surveillance, or another form of financial oppression. Bitcoin stops third parties - including corporations and governments - from oppressing its users.

Therefore:

C3. Disagree. Bitcoin enables its users to "store their value" outside the reach of individuals and institutions.

Initial Claim:

@22:53-23:34

Peter Schiff: "Even if you assume, "okay, cryptocurrencies are going to work," I cannot think of an example throughout history where any innovation- where the first one was the best one, right? Whatever was invented, whether someone invented the telephone- the first telephone was not the best telephone - it's been improved upon. The first television, the first automobile.

So if cryptocurrency would work, why would we assume that Bitcoin is the one that's going to succeed? Why would the first attempt be the best attempt? Why wouldn't somebody come up with something better, that's quicker, that's more reliable, that's more secure than Bitcoin? And if somebody can do that, then it renders Bitcoin worthless because there's something better."

P1. It is extremely unlikely that the first version of a product is the best version of that product type. P2. Bitcoin is the first version of a product type. Therefore: C3. It is extremely unlikely that Bitcoin is the best version of that product type.

Evaluation:

P1. Agree.

P2. Agree.

Therefore:

C3. Agree.

P4. If someone invents a superior version of Bitcoin, then Bitcoin will be worthless. P5. Someone will invent a superior version of Bitcoin. Therefore: C6. Bitcoin will be worthless.

Evaluation:

P4. Disagree. This Premise assumes that only ONE product can retain value in a given marketplace (which requires that all consumers switch to using the one, single, "best" product), which is a False assumption.

Clearly, there is more than one type of telephone that exists today, just as there's more than one type of television, type of automobile, and type of money.

In all likelihood, many cryptocurrencies will exist simultaneously, each with a different use case, market segmentation, and market capitalization.

If someone invents a "superior" version of Bitcoin, then Bitcoin will become less valuable.

P5. Dubious. The label of "superior" is completely subjective, and every product-maker (in every market) must consider various tradeoffs in product design and functionality.

In cryptocurrencies, there is a 3-way tradeoff among security, scalability, and decentralization - you can pick at most two. Bitcoin attempts to have "unrivaled" security and decentralization, and it chooses to sacrifice its scalability. Other cryptocurrencies attempt to favor scalability, for example, at the expense of either security or decentralization.

Therefore:

C6. Agree, but for different reasons.

Bitcoin will become "less valuable" if and when a "superior" version is released.

Bitcoin will become "worthless" when its utility disappears (i.e. its security is compromised). This will not be a function of the competitive landscape (e.g. "other cryptocurrencies"), but rather the technological landscape (e.g. "disruptive technologies," such as quantum computing).

P1. Anything with no intrinsic value is essentially worthless. P2. Bitcoin has no intrinsic value. Therefore: C3. Bitcoin is essentially worthless.

Evaluation:

P1. Disagree. Suppose we define "intrinsic value" as "the benefit derived from the minimum functional properties of an asset that are universally recognized and broadly applicable." In other words, "intrinsic value" is the "objective functionality" of an asset. That seems fair, but this definition causes us to dismiss other kinds of value as "worthless" (such as aesthetic or sentimental value), and clearly those types of value are not worthless.

If we expand the definition of "intrinsic value" to include aesthetic or sentimental value, then we've introduced subjectivity into the core value of something. Since subjective value, by definition, is a matter of opinion, and since we cannot make claims about other people's opinions, then the presence of subjectivity prevents us from making claims about this kind of value.

Hence, this latter definition of intrinsic value (that includes subjectivity) leads to a False Premise because it precludes us from making claims about other people's value, and the former definition of intrinsic value (that is strictly objective) also leads to a False Premise because it ignores a very real component of value (i.e. aesthetic or sentimental value).

Either definition of "intrinsic value" leads to a False Premise, so I Disagree with Premise 2.

P2. Disagree. Bitcoin does, in fact, have intrinsic value. In order for you to "have" a Bitcoin, the Bitcoin network must acknowledge that you have custody of that Bitcoin (i.e. you must supply a valid private key to claim ownership of a balance in a public address).

If you can demonstrate ownership, then you can transfer ownership - without any additional permissions or paperwork. The two functions (demonstrating and transferring ownership) are "structurally connected."

The intrinsic value of a Bitcoin, therefore, is the ability to establish and transfer ownership of digital assets on a globally-recognized and un-cheatable ledger. In other words, once you own something on the Bitcoin network, nobody can take it away, except you (either your own choice or your own negligence).

Another way to consider this intrinsic value is that each Bitcoin user has the same "power" and "sovereignty" as the other users. There is no hierarchy of power - such as authoritarian governments, remorseless corporations, and powerless individuals - there is only a public address with a private key, and everyone on the network is the same. It is an amazing environment of equality, and it's built into the network - if you "have" a Bitcoin, you "have" this equality.

Therefore:

C3. Disagree.

Initial claim:

@14:20 - 15:36

Anthony Pompliano: "Money is just a belief system, right? So a "medium of exchange" is simply valuable because both parties agree [that it's valuable], right?"

Peter Schiff: "Not real money. You're talking about fiat money. You're talking about paper currency that governments create out of thin air. There, [with paper currencies] the value's derived from faith and confidence, but it also has the backing of the government that issued it, and the fact that each government demands that its citizens pay taxes in that currency that it creates, which means that there is a demand among the citizens to accumulate that currency in order to pay those taxes.

And because of that, all of the contracts are denominated in that - employment contracts, rental agreements, bonds, insurance contracts - so everybody starts using it, but ultimately if the government abuses the privilege of creating it, and it creates too much, it collapses in value because the confidence is destroyed.

And Bitcoin has much more in common with a fiat currency than it does with gold, because gold's value is derived from its physical properties that make it desirable and make it useful, whereas Bitcoin's value is derived from the confidence that people are going to want it in the future even though it has no physical properties or any other properties that you could use it for."

P1. If a "medium of exchange" derives its value from its physical properties, then it is "real money." P2. Gold is a medium of exchange that derives its value from its physical properties. Therefore: C3. Gold is "real money."

Evaluation:

P1. There's a lot to clarify here, but such clarification is not essential to the main argument, so let's assume that I Agree with this Premise.

P2. Again, we could clarify this, but it's not essential, so let's assume that I Agree with this Premise.

Therefore:

C3. Agree. Gold is "real money."

P4. If a "medium of exchange" derives its value solely from the "confidence" that people are going to want it in the future, then it is "fake money." P5. Bitcoin is a medium of exchange that derives its value solely from the "confidence" that people are going to want it in the future. Therefore: C6. Bitcoin is "fake money."

Evaluation:

P4. Let's suppose I Agree.

P5. Disagree, but if we include a very important addition, I would Agree:

Bitcoin is a medium of exchange that derives some of its value from the "confidence" that people are going to want it in the future.

Consider that a holder of any non-consumable asset - e.g. stocks and bonds, but also gold and Bitcoin - is reasonably "confident" that people are going to want that asset in the future.

This confidence is a component, but not the entirety, of each asset's value.

Bitcoin is a medium of exchange that derives some of its value from the "confidence" that people are going to want it in the future.

Therefore:

C6. Disagree. Bitcoin is not "fake money."

P7. Eventually, the value of "fake money" will collapse when confidence is destroyed. P6. Bitcoin is "fake money." Therefore: C8. Eventually, the value of Bitcoin will collapse when confidence is destroyed.

Evaluation:

P7. Agree. Eventually, the value of "fake money" will collapse when confidence is destroyed.

P6. As we discussed above, Disagree. Bitcoin is not "fake money."

Therefore:

C8. Disagree, but if we include a very important addition, I would Agree:

Eventually, the value of Bitcoin will collapse when (1) its utility disappears AND (2) confidence is destroyed.

In the short term, macro and micro factors will increase and decrease the overall "confidence" in the Bitcoin network, while the "utility" of a Bitcoin remains unchanged.

In the long term, something will undermine the integrity of the Bitcoin network (e.g. breaking the hashing algorithm, a 51% attack, etc.), and the "utility" (i.e. security) of the Bitcoin network will disappear. When this occurs, people will lose confidence in Bitcoin rapidly, and the value of Bitcoin will collapse.

The same process will unfold in other asset classes (e.g. stocks, bonds, and gold), but on very different time scales (e.g. decades, centuries, or millennia).

P1. A "Ponzi Scheme" is a community, organization, or system characterized by (1) participants who join for a "small" cost and who hope to leave with a "large" profit, and (2) a pool of money which is ultimately insufficient to provide all members with the desired profits, thereby leaving many participants with sizable - and sometimes total - losses. P2. The Bitcoin community exhibits the characteristics of a Ponzi Scheme. Therefore: C3. Bitcoin is a Ponzi Scheme.

Evaluation:

P1. Disagree. This is a loosely accurate example of a Ponzi Scheme, and it bears a superficial resemblance to Bitcoin, but when we clarify some important details, it becomes clear that "a Ponzi Scheme" and "the Bitcoin network" are two very different things. A Ponzi Scheme includes the following features:

P2. Disagree. Bitcoin does not fit the original definition or the improved definition of a Ponzi Scheme. There is no central authority, there's no promise to receive funds in the future, and there's no mechanism whereby a "central authority" attempts to grow the money you paid them when you first acquired your Bitcoin.

People may hope to make a profit from buying and selling Bitcoin, but hope is something that exists inside a single person: a promise is something that exists between two people. There are no promises in Bitcoin, and there's no on-going financial relationship. Without this on-going financial relationship, there's no Ponzi Scheme.

While it's true that many Bitcoin users are attempting to "join for a 'small' cost and... leave with a 'large' profit," this is insufficient to establish Bitcoin as a Ponzi Scheme. In fact, every major asset class includes speculators, who, by definition, are hoping to "buy low, sell high." The presence of speculators in a market does not affect the nature or legitimacy of the asset(s) in that market.

Therefore:

C3. Disagree.

Initial claim:

@22:38 - 22:57

Peter Schiff: "If you [have] Bitcoin, you have nothing. If you divide it into two halves, you have half of nothing. So you're not "dividing" anything. You're not "storing" anything. When [someone] says, "it's a store of value": you must have value in order to store. Bitcoin has no value today - there's nothing you can do with it, so it doesn't make sense for you to store it for the future, because there'll be nothing you can do with it in the future either."

P1. For something to have value, it must have "utility" (i.e. the ability to accomplish something useful or practical). P2. Bitcoin has no utility. Therefore: C3. Bitcoin has no value.

Evaluation:

P1. Dubious, but let's suppose we Agree. (I would tend to argue that anything can have value under the "right" conditions, but we can overlook that point for this Argument).

P2. Disagree. Bitcoin does, in fact, have utility (i.e. the ability to accomplish something useful or practical).

The Bitcoin network provides a solution to each of the following problems:

Of course, there are some existing solutions to each of these problems. The point here is not that Bitcoin is unique in solving these problems, but rather that Bitcoin is simply an "available alternative."

Since Bitcoin provides a solution to at least one problem, then Bitcoin has utility (i.e. the ability to accomplish something useful or practical).

Therefore:

C3. Disagree. Since Bitcoin has utility, Bitcoin has value.

What is the "fair value" of Bitcoin, and is it currently undervalued or overvalued? That question is - and always will be - answered by the sum total of the opinions of every person on the planet: i.e. "the market" and the current market price.

P1. For something to have value, it must be tangible. P2. Bitcoin is not tangible. Therefore: C3. Bitcoin can not have value.

Evaluation:

P1. Disagree. There are many examples of intangible things that have value: love, freedom, friendship, power, memories, promises, and even "the satisfaction of being right." Those are things we live and die for (and often kill for), so clearly, intangible things can have value.

P2. Agree. Bitcoin is not tangible.

Therefore:

C3. Disagree. Bitcoin can have value.